Alphabet disappoints on sales as ad business slips after pandemic run-up

Alphabet Inc on Thursday posted fourth-quarter profit and sales short of Wall Street expectations as Google’s advertising clients pulled back spending from a period of pandemic-led excess.

Executives of the search and advertising giant adopted a subdued tone on a call with investors, promising an extended period of belt-tightening, particularly on hiring, real estate costs and experimental projects that can take years to reach fruition.

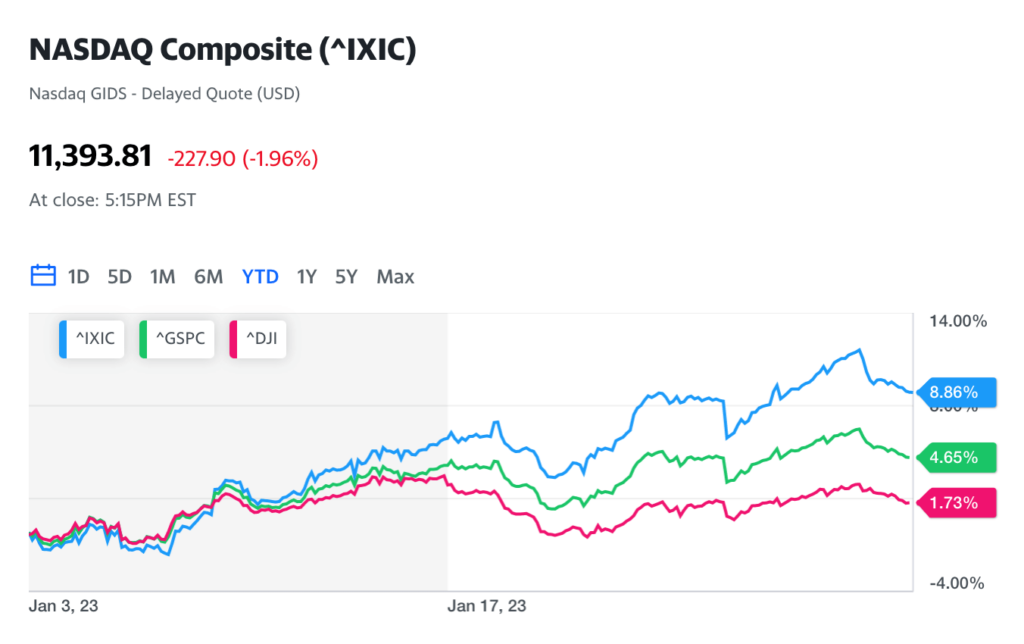

Shares of Alphabet were down nearly 5% in after-hours trading, after losing about 40% of their value in 2022.

“We are committed to investing responsibly with great discipline and defining areas where we can operate more cost- effectively,” Chief Executive Sundar Pichai told analysts on a call to discuss the company’s results. That echoed comments from Meta Platforms Inc boss Mark Zuckerberg the previous day on cost efficiencies.

Shares of other tech companies Apple Inc and Amazon.com Inc also fell after they posted disappointing results on Thursday, wiping off gains after Facebook parent Meta on Wednesday boosted tech shares with news on cost cuts and a large buyback.

Gone was some of the exuberance of the pandemic when consumers flocked to the internet amid lockdowns and heightened interest in e-commerce and touchless deliveries.

Alphabet’s chief financial officer, Ruth Porat, promised a more measured approach for 2023 and a focus on “delivering sustainable financial value,” not necessarily a hallmark of Silicon Valley firms. “We’re focused on revenue upside as well as durable changes to the expense base.”

Advertisers, who contribute the bulk of Alphabet’s sales, have cut their budgets as rising inflation and interest rates fueled concern over consumer spending.

Pichai pointed to advertisers’ more modest spending and the impact of foreign exchange rates abroad as drags on Alphabet’s overall results.

He said artificial intelligence (AI) software will be an important focus for the company and that it plans to make its LaMDA chatbot software publicly available in the coming weeks.

LID ON COSTS

Mountain View, California-based Alphabet decided to cut 12,000 jobs last month, representing about 6% of its overall workforce, and said it was doubling down on AI. Across the company, Alphabet will “meaningfully” slow its pace of hiring this year, said Porat.

Alphabet, long a leader in AI, is facing competition from Microsoft Corp, which is reportedly looking to boost its stake in ChatGPT – a promising chatbot that answers queries with human-like responses.

“Despite being seen as one of the most insulated companies in the advertising space relative to peers, Alphabet’s poor quarter is the latest sign that worsening fundamentals and a tough macroeconomic environment are prompting advertisers to cut back on spending,” said Jesse Cohen, senior analyst at Investing.com.

Net income fell to $13.62 billion, or $1.05 per share, from $20.64 billion, or $1.53 per share, a year earlier. That was the sharpest decline for Alphabet in four quarters.

Adjusted profit of $1.05 per share fell short of an expected $1.18 per share, according to Refinitiv.

Revenue from Google advertising, which includes Search and YouTube, fell 3.6% to $59.04 billion. Total revenue rose 1% to $76.05 billion, its slowest growth ever barring a small decline in the second quarter of 2020. Analysts were expecting $76.53 billion.

Google is the world’s largest digital ad platform by market share, making it uniquely susceptible to fluctuations in online marketing spending. Its YouTube division has faced a surge in rival platforms, particularly TikTok, whose endless scroll of short video is drawing younger users away.

Alphabet’s Porat said the company’s total capital expenses this year will be in line with last year. As more of its employees work remotely and it consolidates staff, Alphabet expects to pare back its real estate expenses, which Porat said would result in a charge of roughly a half-billion dollars in this year’s first three months.

Revenue from YouTube ads, one of Alphabet’s most consistent money-makers, fell nearly 8% to $7.96 billion, well below the estimate of $8.25 billion, according to FactSet.

Cloud was a bright spot, however, with revenue growing 32% to $7.32 billion, but at its slowest pace since the company began disclosing the segment’s revenue numbers.

But there may be more pain ahead for Alphabet. Late last month, the Justice Department and eight states sued Google over what they said were anticompetitive practices in its digital ad sales. The company is facing multiple lawsuits, which, if successful, could cause it to be broken up.

Source: finance.yahoo.com